Jason M. Barr January 29, 2024

[Coming May 14, 2024: Cities in the Sky: The Quest for the the World’s Tallest Skyscrapers (Scribner Books)]

What’s driving the affordability problem in New York City? If you ask a random person on the street, they’ll blame developers, who seemingly only build luxury towers for the well-to-do. But the developer might say that the land values are to blame—to recoup the high cost of the land and expensive construction costs, the only profitable new development is on the high end.

As discussed in the previous post, expensive land values are a symptom—not the cause—of a larger problem—the lack of land being offered up for redevelopment. The high land values signal New York’s “scarce land policy.” The lack of in-fill and densification is due to a series of government-made and natural frictions. Here we dive into more details about the nature of these frictions and the policies needed to “loosen” things up.

Gummed-up Gotham

First, let’s review the facts on the ground. If we look at block-level changes in the number of housing units in the last two decades, we see a very sticky Gotham. Nearly one out of three (31%) blocks with at least one housing unit in 2004 had no change in the number of units since then. 57% of blocks had zero, plus or minus one unit. More broadly, nearly half (48%) of the city’s blocks had no change or lost units. No matter how you slice and dice it, about half of the city’s residential blocks remained frozen in the last two decades.[1]

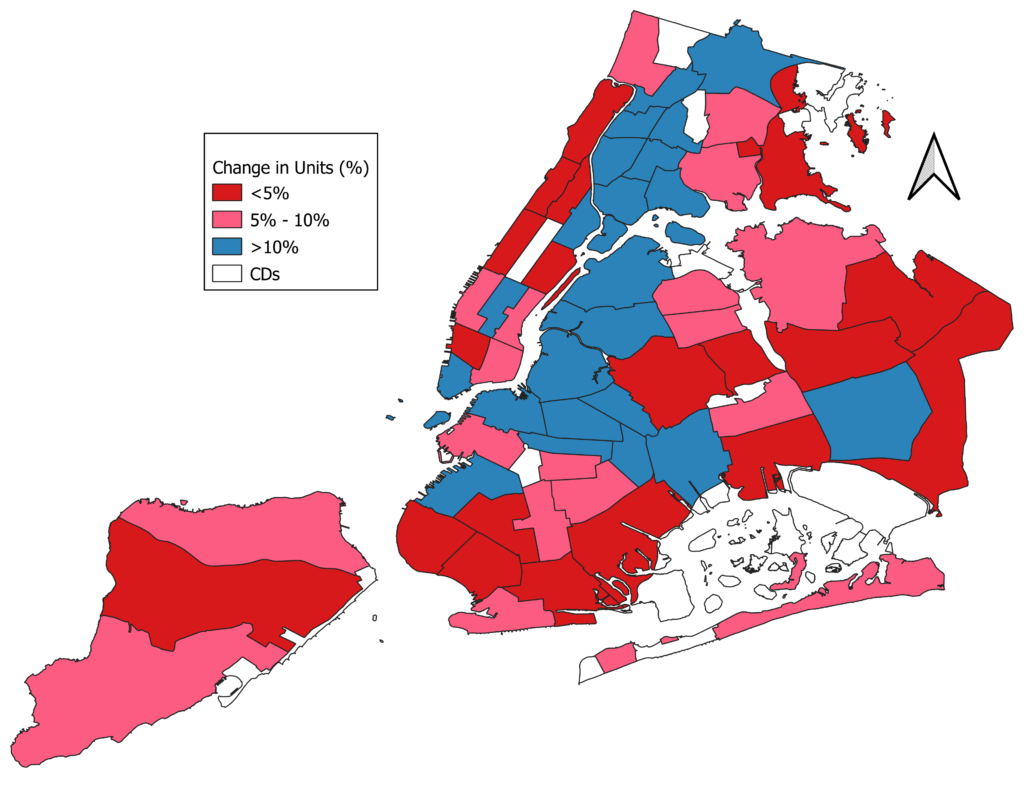

Taking a helicopter view of New York’s 59 community districts, nearly two-thirds grew their housing by less than 10%, while only four had a two-decade growth rate of 30% or more (see figure below). In short, only four community districts did any real heavy lifting, and one was lower Manhattan, where Art Deco office towers were converted to apartments.

Should I Stay or Should I Grow?

New York City has about 859,000 land parcels (and the number has been steady over the last few years). One metric of what’s offered for development is to count the number of new building permits for housing.

In the last five years, the average number of permits issued is about 1,500 per year, and the city has completed, on average, about 25,000 per year or about 250,000 gross new housing units per decade—without accounting for teardowns, unit mergers, or conversions to other uses. 2023 was a terrible year, with less than 10,000 units permitted. A back-of-the-envelope calculation suggests that the probability that any lot “gives itself up” for redevelopment is about 1,500/859,000 = 0.17%.

One year ago, Mayor Adams proposed adding 500,000 units in the next decade which would represent a nearly 250% increase in the number of units built each year and more than double the number of permits issued. But we can’t get to abundant housing if the land is iced.

Give Yourself Up

The aim of this post is to estimate the probability or likelihood that a block generated at least one new unit of housing over the five years from 2018 to 2022 based on the block-level characteristics that existed as of 2016.[2] In short, the exercises aim to look at what features of New York’s lots and blocks are incentivizing or disincentivizing new construction. (The data sources and processing are here.)

This statistical exercise does not consider things like tax abatement generosity or broader macroeconomic issues like rent values. Rather, the analysis considers what is about the lots and blocks themselves and the buildings on the lots that would suggest why a lot is given up. If we genuinely want to make housing more affordable, we need to know what’s going on and focus on “loosening” the lots.

Probably?

The data reveal that the probability of a city block producing at least one unit of new housing (given it had at least one unit previously) during the period was about 13% or about 2.6% per year. These blocks produced about 48,000 new units or about 9,600 per year (which also suggests that about half of all new housing built today is on formerly commercial, industrial, or vacant land).

So, let’s say, for example, to get to more abundant housing, we want to double the probability that a block produces at least one unit of new housing. What would it take? In other words, how do we go from a five-year probability of 13% to, say, 25%?

Drivers of the Gap

As discussed in the prior post, the underlying economics of cities and land use suggest several factors that drive the likelihood that a lot will have redevelopment. I defined the “Development Gap” as the potential profits obtained from densifying a lot versus the profits from keeping the lot as it is. The higher the Gap, the more likely a lot will gain more units. What are those elements?

Centrality

The first is centrality. Since housing prices are higher in the center because of the greater demand to reside there, the Gap will be higher in more central locations (here, I define the city center as the Empire State Building).

Zoning

Next is zoning regulations—the more stringent the regulations, the lower the Gap because the redevelopment floor area is capped to something that would not produce an income above the cost. In New York, building density is regulated by caps on the Floor Area Ratio (FAR), which limits total floor space per square foot of lot area. In many instances, a current building’s floor area is greater than the allowable maximum for a new structure, making redevelopment virtually impossible.

Current Building Density

The greater an existing building’s density and height, the less likely the lot will be redeveloped because of the difficulties associated with emptying and tearing it down.

Rent Stabilization

Rent stabilization is a mixed bag in terms of incentivizing redevelopment. On the one hand, it lowers the actual income relative to the market-rate potential. On the other hand, it’s hard to redevelop when it’s difficult to get tenants to move. So, the net effect is unclear a priori.

Ownership Status

Turning to owner-occupied units, we expect those to be much less likely to be redeveloped. In the case of condos or coops, all the tenants would have to agree to such an idea—nearly an impossibility. In the one- or two-family-home case, homeowners are less likely to move, given the costs of selling their house and buying a new one. Additionally, homeownership is highly subsidized to encourage long-term tenancy. So, homeowners, by their very nature, are households that are less likely to move.

Landmarking and Historical Districts

Landmarking and historical districts reduce redevelopment because they make it illegal to make large-scale changes to the affected properties.[3]

Call Me Maybe: The Evidence

Policy Created Frictions

Turning to the statistical (regression) results (here), I find that the “Development Gap Theory” is strongly supported. Scarce housing in New York is not a mystery: Economics matters and the way to get more supply is to understand the factors that disincentivize new housing—across the entire city.

Regarding policy decisions, zoning strong impacts redevelopment. For example, the analysis reveals that doubling the allowable FAR on a block (e.g., from 1 to 2 or 2 to 4) increases the probability of redevelopment in five years by about ten percentage points. Relatedly, the more lots on a block above the allowable FAR, the lower the probability of redevelopment, as expected. Each additional ten buildings over the allowable limit reduced the likelihood of redevelopment by about 1.5 percentage points.

As expected, the statistical analysis shows that the more buildings that are landmarked or fall within historic districts, the less likely a block will have new residential buildings five years later, similarly for blocks with many owner-occupied units.

Interestingly, a block with more rent-stabilized buildings does not affect the probability that a block will create at least one unit. This likely reflects how rent stabilization impacts the Gap, as discussed above.[4]

Natural or Structural Frictions

But policy decisions about land use are not the only game in town. As cities age, they create their own “natural” or “structural” frictions. In principle, the city’s grid can determine the shape of the blocks and the number of parcels on each one. Over time, ownership can become more dispersed, making combining lots harder. Before zoning, many blocks had buildings with much greater densities. Plus, location matters—places where prices are lower are less likely to redevelop simply because of the economics.

The statistical results here strongly suggest that these historical factors matter. Buildings further away from the center, on average, are less likely to add new housing simply because of the lower revenues these properties will generate. If two blocks are similar, but one has twice the building floor area, its redevelopment probably drops by four percentage points.

Interestingly, larger blocks are less likely to have redevelopment activity, while blocks with more lots will likely see more redevelopment. The reason for these findings needs to be explored further, but having more lots on a given block means more decision-makers, and thus, it is more likely that some of them will redevelop their properties. Lot size matters, too. If a block has too many very small lots, it’s less likely to see redevelopment.

Playing the Odds: Getting to Abundant Housing

Given the findings, what might the City do to double the probability of getting double the housing?

Upzoning

Let’s start with zoning. The evidence worldwide shows that upzoning works, and the data analysis here also supports that. I found that stringent zoning strongly reduces the probability that a block will build new housing.

Say the city doubles the allowable floor area ratio (FAR) on each block and that none of the buildings are above the allowable floor area. This change would increase the five-year citywide probability of redevelopment by an additional ten percentage points. So, doubling zoning gets you about three-quarters the way there.

Taxing and Subsidies

Construction subsidies or tax abatements can help loosen up the lots, but they need to be more targeted to “stickier” areas. They should be based on the distance from the center or the neighborhood’s income level. Lower-income neighborhoods should get more generous subsidies, as should those further away from the center. For single-family districts, the city should give tax abatements for ADUs or converting single-family housing into two-family housing.

New York City has over 565,000 one- and two-family homes. As a thought experiment, if each added one more unit—an Accessory Dwelling Unit (ADU) or new internal unit via subdivision—the city could get to Mayor Adam’s target of 500,000 new units without a single teardown.

More broadly, a land value tax that taxes land values higher than the value of the building is a good way to disincentivize the holding of under-developed plots.

Land Banking

The City can’t do much about block sizes and current building densities. However, it can impact zoning regulations and encourage land assembly or land banking. The City would buy up underutilized lots and then sell them to other property holders on the block creating larger lots that would be more profitable to redevelop.

A City of Yes?

Mayor Adams likes to use the phrase “City of Yes” to pitch his plans for new housing, but today Gotham remains the “City of No.” The road to abundant housing is clear:

- Relax stringent zoning rules (especially near transit lines),

- Subsidize housing construction costs in lower-income housing neighborhoods and those in “low Gap” neighborhoods.

- Allow one- and two-family homes to add one or two more units.

- Create a land value tax.

- Establish a City authority that buys land to encourage land assembly or sells ground leases for affordable development.

Despite widespread supply skepticism, the results in this post show that the problem of affordable housing is not one of economics—it’s one of politics. Releasing the land will get us there if the political will emerges to allow it. It’s time to unstuck Gotham.

Continue reading Part I of the series here.

—

[1] These statistics are based on lots that had some housing units in 2004. Thus, we are not talking about the conversion of industrial or commercial land to residential.

[2] I repeated the exercise to see what prompts a block to build ten or more units of new housing. Results are broadly similar. See here for the results.

[3] I want to be clear, I’m not opposed to landmarking and the creation of historic districts. However, it’s important to recognize that they reduce a city’s ability to provide more housing supply.

[4] However, the more rent-stabilized buildings on a lot, the more likely it will be redeveloped for ten units or more. So, it suggests that rent stabilization is promoting redevelopment in denser, more central places where the Gap is stronger.

“Rent Stabilization

Rent stabilization is a mixed bag in terms of incentivizing redevelopment. On the one hand, it lowers the actual income relative to the market-rate potential. On the other hand, it’s hard to redevelop when it’s difficult to get tenants to move. So, the net effect is unclear a priori.”

I have been developing in NYC for 40 years. I don’t understand your comment on Rent Stabilization. It is the elephant in the room. In other cities an owner can just stop renewing leases to vacate a building, tear down and build to maximum zoning. In NYC, the process is extremely expensive and arduous and only economically possible for the highest value sites. Do a search of hold out tenants who are paid millions to relinquish their rent stabilization rights. This after years of negotiation to buy out the tenants from their leases. This accounts for a high percentage of the blocks where not a single new unit has been produced for decades. And it wouldn’t change if you upzoned the block unless the block is in a highly desirable location – luxury stuff.

The only positive of rent stabilization for developing more housing is that it accompanies the provision of real estate tax exemptions which are necessary to make the numbers work for all but the most luxurious housing.

I agree with your comments. But my question was this: Statistically speaking, are parcels with rent-stabilized more or less likely to be redeveloped as compared to properties with no rent-stabilized units, all else equal? The point is that economically speaking, on the one hand, the fact that it’s expensive to empty a rent-stabilized building means it’s difficult to redevelop the property. However, when the difference between the possible market rents and current rents is large, it incentivizes property owners to redevelop the property and pay the costs (e.g. in MN south of 96th St). When I crunch the numbers, the data suggest that the two effects, on average, seem to cancel out, so that rent-stabilized buildings are no more likely to be redeveloped than other parcels (again holding all other factors, like zoning, constant). If you relaxed zoning rules and allowed property owners to not renew leases, then, yes, you would see more redevelopment of these sites. In the larger scheme of things, rent stabilization is one of several “frictions” that gum up the NYC real estate market. Just as important is that nearly half of the city’s residential land has a maximum allowable FAR of less than 1 (is the outer ring of the city).

https://therealdeal.com/new-york/2024/01/30/gary-barnetts-holdout-will-not-fold/